This article originally appeared at Engine.is

Yesterday, the Bureau of Labor Statistics released its much anticipated jobs report for the month of September–more than two weeks late because of the federal government shutdown. Maybe lawmakers were trying to do us a favor because this wasn’t a great report. The unemployment rate ticked down to what is still an unacceptably high 7.2 percent, while employment grew just enough to keep up with population growth. In fact, the employment-to-population ratio remains stuck in about the same place it was nearly four years ago. These are not signals of a robust jobs recovery.

Because I’m interested in employment, economic progress, and the technology sector as a key driver of growth, I used this occasion as an opportunity to look at recent employment trends for this high-value segment of the economy. What I found surprised me.

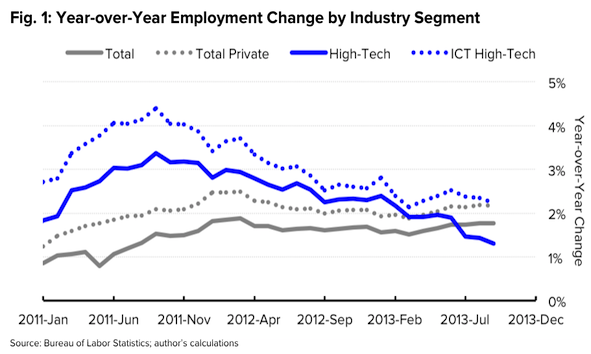

Figure 1 shows that since peaking at an annual growth rate of 3 percent in September 2011, employment growth in the high-tech industries has steadily slowed to about 1.6 percent two years later. This matches the employment growth seen across the entire economy but falls below the rate seen for the private sector.

This trend was even more pronounced for the ICT segment of high-tech, which includes firms in computer hardware and software, information services, and Internet infrastructure (this excludes the pharmaceutical and aerospace manufacturing, and engineering and scientific R&D services industries included in the broader high-tech sector). The year-over-year ICT high-tech job growth rate eclipsed 4 percent in mid-2011, but has since fallen to 2.3 percent.

Another way to look at the high-tech workforce is by occupation–particularly because we define the high-tech industries by their concentration of workers in the STEM occupations of science, technology, engineering, and math. Since nearly 44 percent of all STEM workers are employed in the high-tech sector, that leaves millions of additional technology-oriented workers employed in other industries to look at.

In that spirit, Figure 2 shows the year-over-year percentage change in employment for the STEM occupations versus all occupations since the beginning of 2011. Because these data are noisy, I also include a data filter to establish a more visually accessible trend.

Here, we see a fairly similar trend: growth, but a slowdown in that growth. Despite a sharp uptick in recent months, the overall trend for these highly-technical high-value jobs is a clear slowing of growth, and convergence with the anemic growth rates for all occupations across the entire economy.

To get a sense of how these trends fit into other measures of economic vitality, I took a quick glance at equity price performance and venture capital investments. It’s a little bit of a mixed bag, but these measures do not contradict what the jobs data show. For example, S&P tech stock indices have slightly underperformed the broader S&P 500 index in the last two years, and after adjusting for inflation, venture capital investmentshave been flat.

Economic output data–which measure an industry’s contribution to GDP or national income–are too lagged to analyze here, but that data could help us understand whether it is the tech sector that is slowing down, or if it has been able to continue producing with fewer workers, with less investment, or at lower valuations.

While pinning-down exactly what is happening requires a more thorough analysis than is offered here, any slowdown in this segment of the economy would be problematic: the tech sector fuels innovation, its goods and services make other sectors more productive and improve the lives of consumers, and it is a critical source of national income.

I have previously documented the high-value nature of technology workers, the pervasiveness of the growth potential in this segment, and the secondary economic benefits they can bring to a region. We simply cannot afford a slowdown in our high-tech sector or its workforce–particularly as the U.S. economy continues to grind out another jobless recovery.